Ireland's Shadow Budget

We forgo billions a year in tax breaks with little scrutiny or oversight

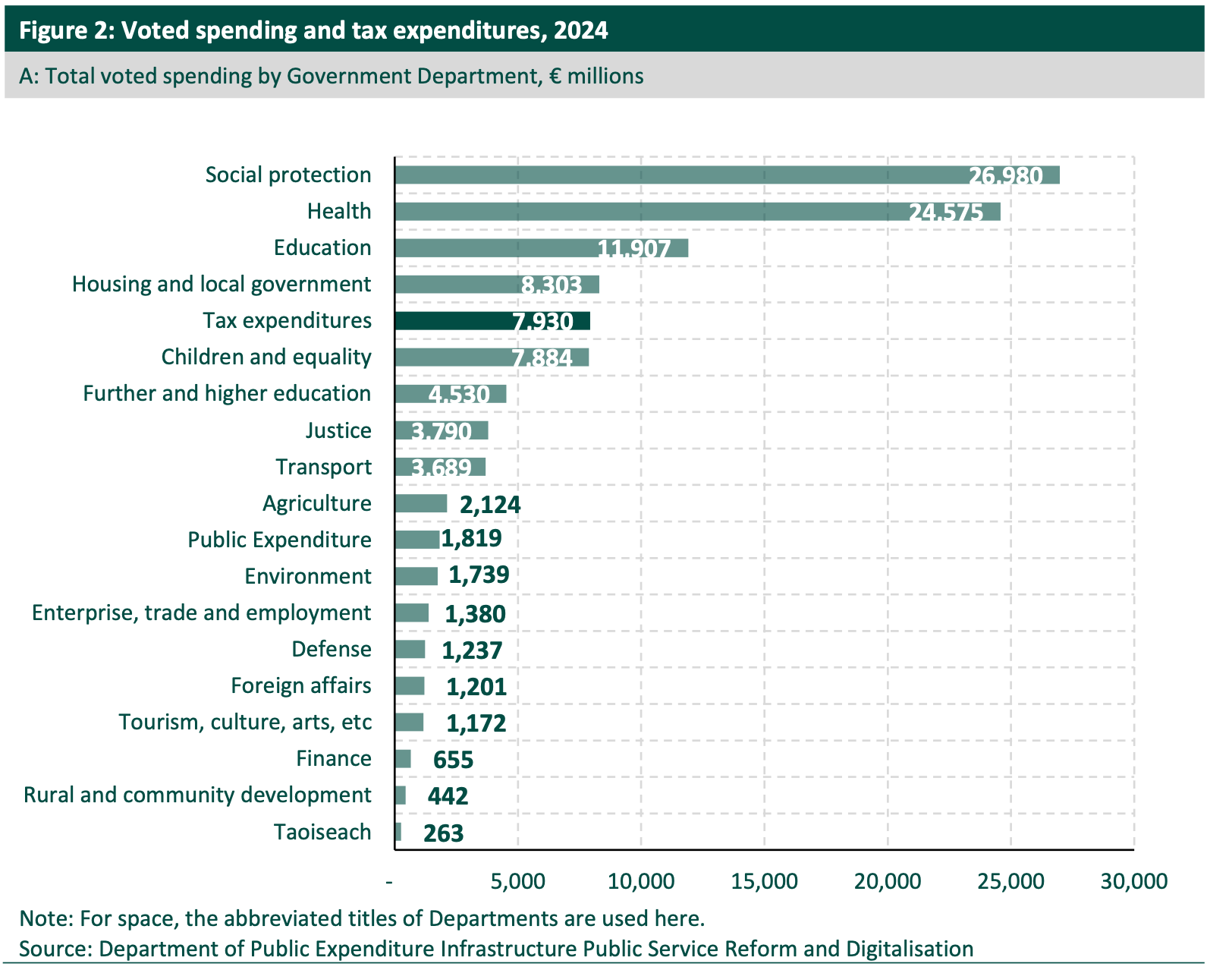

Each year, Ireland quietly forgoes more revenue in tax breaks than most government departments spend: €8 billion in 2024 according to the Department of Finance’s own estimate. This amounts to around 2% of national income, more than the total voted expenditure of all but the Departments of Social Protection, Health, Education and Housing.

Yet these tax breaks - also known as tax expenditures - are not subject to the same degree of scrutiny typically applied to direct expenditure. We lack even basic information like the estimated cost or number of beneficiaries for many (the €200,000 tax-free pension lump sum, for example).

Poor evaluation culture

There is also a poor culture of evaluating whether tax expenditures are meeting their stated objective (let alone whether that objective is sensible). Many tax expenditures have never been subject to an evaluation since they were introduced, while others have not been subject to any evaluation for at least a decade.

Moreover, most of the evaluations of tax expenditures that have been carried out are of exceptionally poor quality. Many effectively amount to asking beneficiaries if they would like to continue receiving tax relief (e.g. the most recent Department of Finance evaluation of SARP - the Special Assignee Relief Programme).

This is not to say there isn’t a role for tax expenditures in pursing policy aims. But our weak evaluation culture and lack of scrutiny means we have little idea whether tax expenditures are achieving their stated aims or whether they represent value for money compared with alternative measures.

This should be of particular concern given that many tax expenditures are uncapped with the cost highly concentrated among a small number of beneficiaries. For example, Revenue estimate that the 782 claims for Capital Acquisitions Tax business relief cost €430 million in 2024. This means the relief was worth around €550,000 per claim on average, and so that the average beneficiary was inheriting a business valued at more than €1.6 million: 37 times the CSO’s estimate of the median value of self-employed business wealth. This suggests the relief mainly benefits those inheriting large rather than small family businesses.

These were some of the main points I made to the Oireachtas Committee on Budgetary Oversight yesterday, where I appeared to discuss the topic along with Dr. Micheál Collins of UCD and two researchers from the Zurich based Tax Expenditures Lab. A transcript of that discussion should be available here on the Oireachtas website in a couple of days (understandably the proceedings in the Dáil and Seanad get priority) while a recording is available here (from about 19 minutes onwards).

Doing better

Much of that discussion was given over to talking about how we can do things better. I suggested the Committee might want to consider some of the recommendations of the previous Government’s Commission on Taxation and Welfare (of which I was a member), notably:

The inclusion of sunset clauses for all new – and existing – tax expenditures to provide a statutory basis for regular review;

Expansion of dedicated economic evaluation capacity within the Department of Finance to work specifically on tax expenditures, and whose work should be peer-reviewed by an outside body;

The provision of forecasts for tax expenditures in annual tax expenditure reports

Like most of the recommendations made by the Commission, these suggestions have been ignored. Unlike many of the recommendations made by the Commission, these shouldn’t be controversial. Rather, they should be the minimum scrutiny we expect of the billions we spend each year on tax breaks.